Byline trends in the media

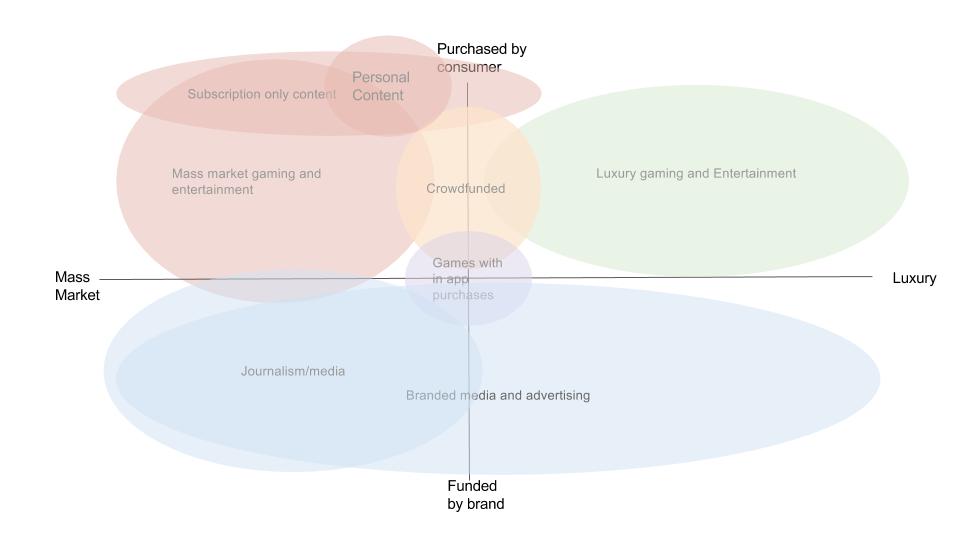

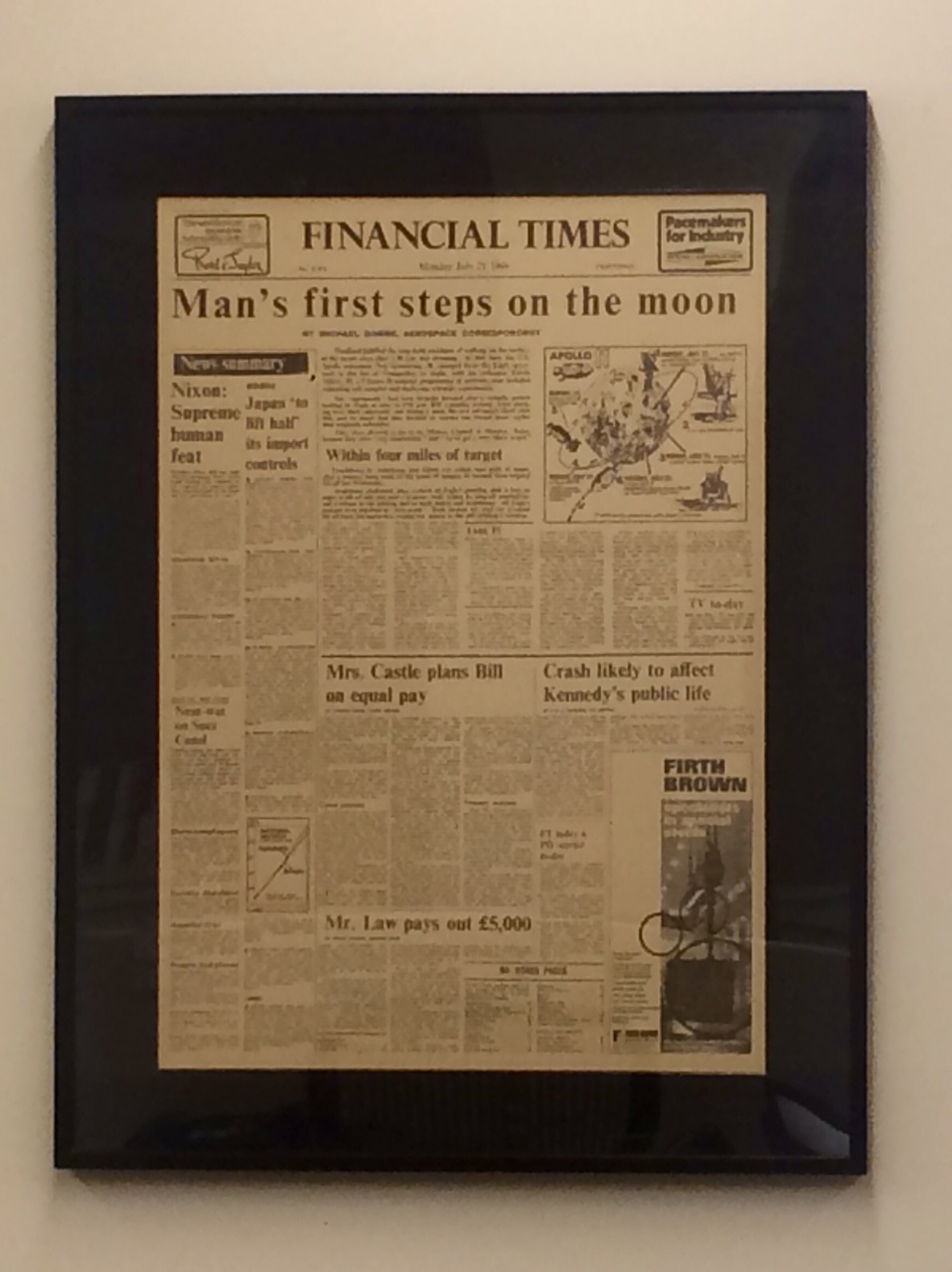

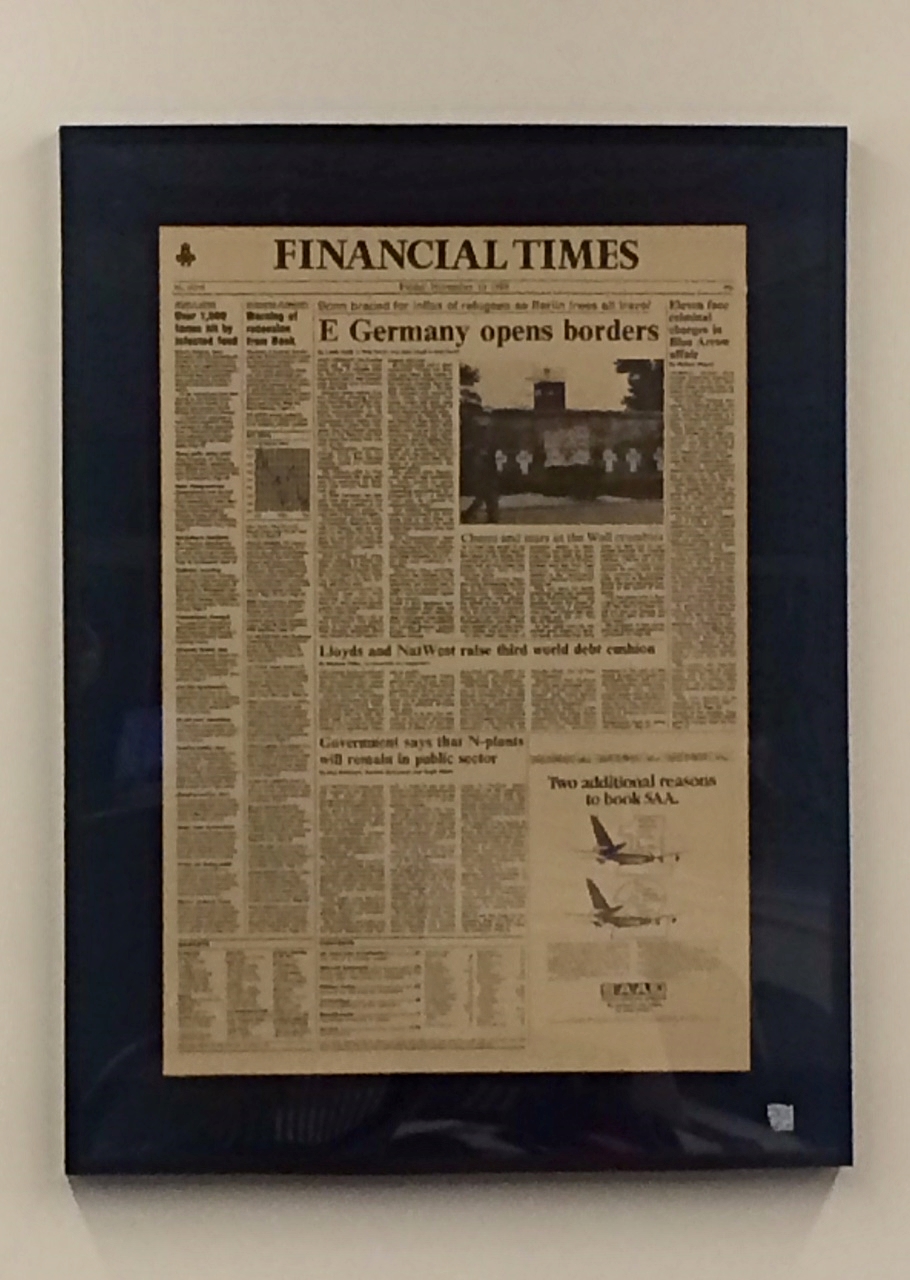

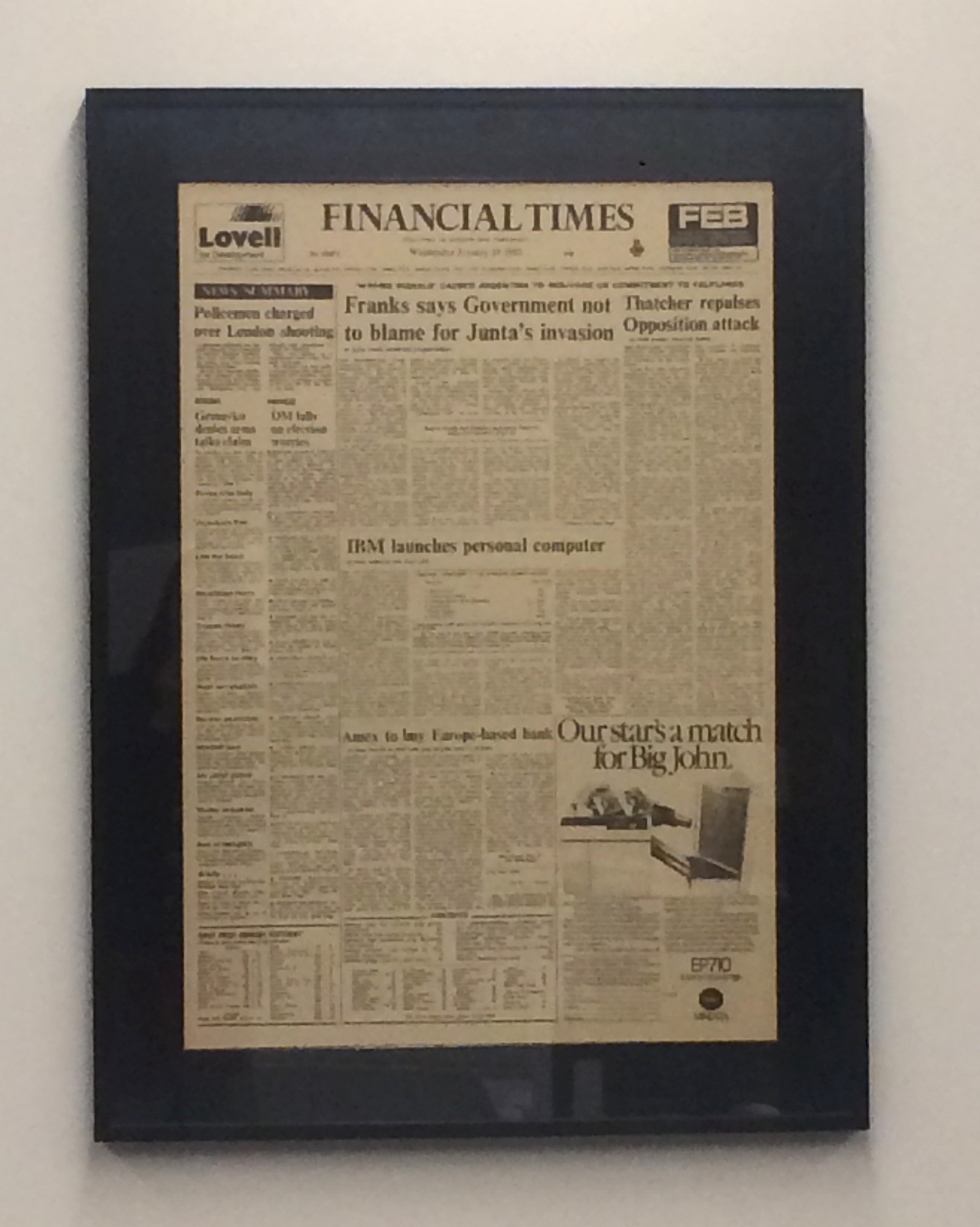

My desk at the FT faces a number of historical front pages chosen to document major world events. Interestingly, these pages reveal more than just the news of that day. There is a trend that emerges when you look at them chronologically: the increasing use of bylines over time.

Zvi Reich looked into how and why bylines developed in his 2010 article "Constrained authors: Bylines and authorship in news reporting." According to Reich's research, the development of regular bylining was a four stage process that extended throughout the 20th century. The stages:

- No bylines, in order to have a singular authoritative voice (like the Economist continues to have).

- Generic bylines. For instance listing agency copy to avoid plagiarism and comply with copyright law.

- Bylines to a few, select, staff members. Often for "role distancing." Meaning opinion or analysis pieces were set apart from the news by labeling the author. [Cultural context: this coincided with the rise of TV personalities, and may have been used as a way for print media to compete.]

- Universal bylining.

Reich wrote that universal bylining gave the reporters more power and enabled journalists' "ascent to stardom." This, in turn, gave journalists more power. Indeed, when news is widely available -- as it has increasingly become since the internet -- the journalists and their unique way of telling a story and interpreting an event become an important factor in driving consistent readership.

Interestingly, this power of a byline is likely to become even more true. We now have algorithms and bots which can write a news story. The incorporation of these systems into reporting makes differentiating between the human and the bot more important. Similarly, third party platforms like Twitter and Facebook enable more direct contact with audiences and also help with discovery and the power that journalists --- through their names -- espouse.

This power can be seen in journalists' use of their own names as leverage to develop a new, separate media outlets from where the personality gained his or her following. For instance, consider Ezra Klein and Vox, Nate Silver and 538, Kara Swisher & Walt Mossberg and Re/Code, etc.

This trend, however, is not consistent across the board. Editorials and homepages offer counterpoints.

Editorials -- the publisher's view or take on the news of the day -- are typically unsigned. Yet even here we find the lack of byline is less true than it once was. Most recently, the New York Times has published signed editorials. Here, the Public Editor cites Andrew Rosenthal about the choice:

It seemed to make sense to try signed editorials when they are not really a declaration of policy, but more of an essay, especially on subjects we have covered a great deal... signed ones won’t take positions that contradict those of the editorial board. But we also want to keep looking and moving forward.

This hearkens back to the first stage -- authoritative voice -- but is slowly changing and may follow a different trajectory.

Secondly, this same bylining trend is only partially true online. In the case of the NYT Reich states that "there were substantially more bylines on the front page than on the inner pages." Yet, on the homepage we only see brand journalists and authors -- more similar to the third stage -- but without stage one or two coming first. With the homepage becoming less important, and article pages more important, it will be interesting to see how this changes.

Screenshot taken May 26, 2016 at 2pm mountain time.